S&P500 Trading Update 15/4/26

S&P500 Trading Update 15/4/26

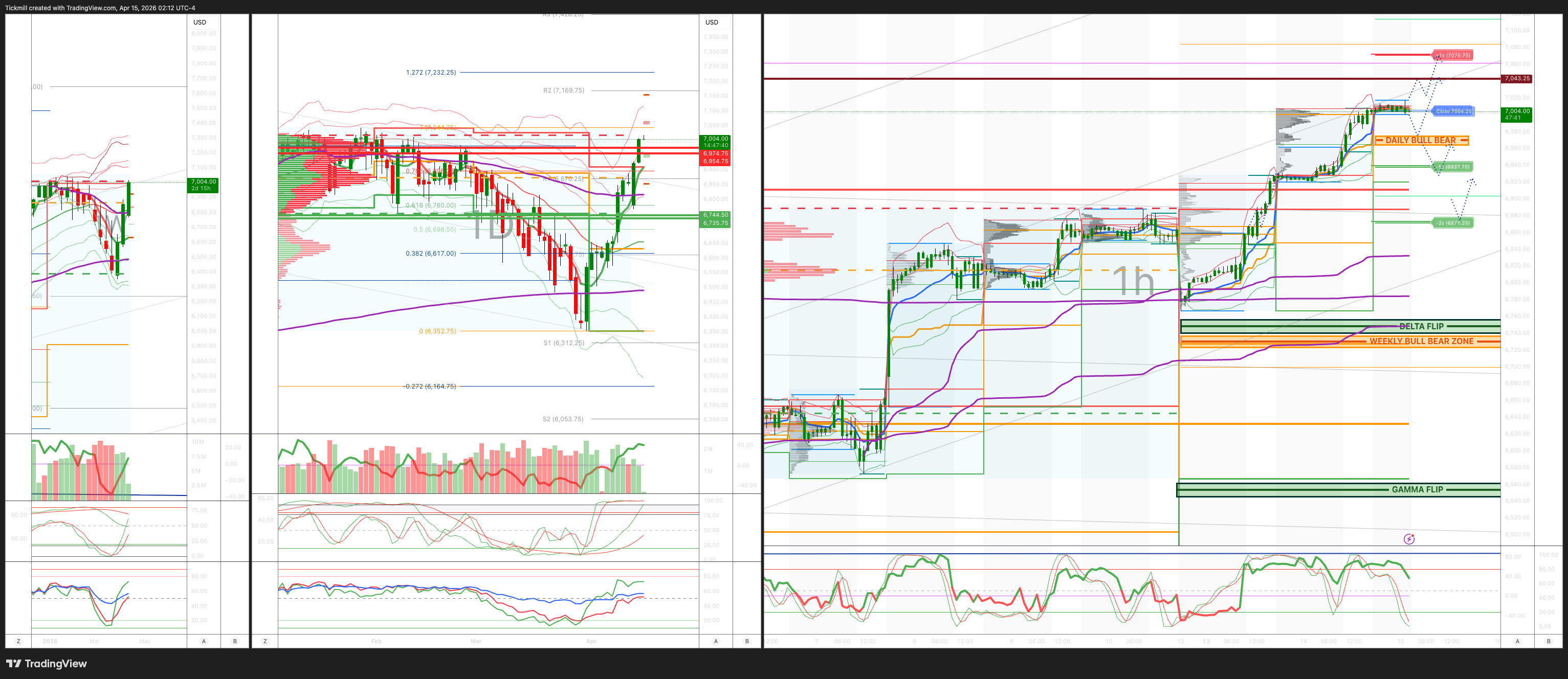

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 6730/20

WEEKLY RANGE RES 6745/35 SUP 6955/75

April OPEX Straddle: 328.55pt range implies a OPEX to OPEX range of [6177, 6835]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 0.92 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 6908

WEEKLY VWAP BULLISH 6637

MONTHLY VWAP BULLISH 6815

DAILY STRUCTURE – OTFH - 6937

WEEKLY STRUCTURE – OTFH

MONTHLY STRUCTURE - OTFD - BALANCE

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Down (OTFD): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 6975/85

GAMMA FLIP 6704

DAILY RANGE RES 7070 SUP 6937

2 SIGMA RES 7137 SUP 6871

VIX BULL BEAR ZONE 22

TRADES & TARGETS

LONG ON REJECT/RECLAIM OF DAILY BULL BEAR ZONE TARGET ATH > DAILY RANGE RES

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Rising Tide’

US Equities Morning Note

US equities extended their rally on Tuesday, with the major indices finishing firmly higher as easing geopolitical concerns, falling crude, and continued strength in large-cap technology supported risk appetite. The S&P 500 rose 1.18% to 6,867, closing with a $400mm MOC buy imbalance, while the Nasdaq 100 gained 1.81% to 25,842, marking its 10th consecutive advance, the longest streak since 2021. The Russell 2000 added 1.32% to 2,706 and the Dow rose 0.66% to 48,536. Total consolidated volume reached 17.9bn shares, below the 2026 YTD daily average of 19.4bn.

The broader cross-asset backdrop remained supportive for equities. VIX declined 3.97% to 18.36, WTI fell 7.0% to $92.13, and the US 10-year yield declined 5bp to 4.25%. The DXY weakened 0.25% to 98.11, while gold rose 2.1% to 4,840 and Bitcoin advanced 1.46% to $74,265. The S&P 500 is now approximately 10% above its March 30 intraday low and closed just below its all-time high of 6,978.

Leadership remained concentrated in higher-beta and AI-linked segments of the market. Speculative growth pockets outperformed, including Quantum Computing (+12%) and Bitcoin-sensitive equities (+5%), while the Mag 7 rose approximately 3% on the day and is now up roughly 15% over the past 10 sessions. Investor focus remains on the durability of AI-related earnings and capex monetisation. In that context, recent support has come from several stock-specific developments: Amazon has benefited from commentary indicating that AWS AI services have exceeded a $15bn annualised run rate, alongside reports that its Trainium chips are being used to train Anthropic’s Mythos model; Meta has been supported by the launch of its Muse Spark AI model, reinforcing The view is that elevated AI spending is beginning to translate into visible model progress, and Broadcom has outperformed since announcing a long-term partnership with Google to develop TPUs through 2031 and expand collaboration with Anthropic.

From a flow perspective, the tone improved further. Desk commentary pointed to continued coverage of index hedges as the geopolitical backdrop stabilised, along with an easing of source-of-funds sales that had weighed on the market through much of the first quarter. Positioning also appears to be turning incrementally more constructive ahead of earnings, while ongoing corporate repurchase activity — including through 10b5-1 plans — remains supportive even during blackout windows.

On the day, internal desk flow skewed decisively to the buy side. While overall activity levels were described as moderate, with the floor rated at 4/10 for activity, the desk finished +684bp to buy, versus a 30-day average of -12bp. Asset managers were large net buyers, with demand spread broadly across sectors, led by Technology, Financials, Communication Services, and Health Care. Hedge funds were modest net sellers, driven primarily by supply in Energy.

In macro, March PPI rose 0.5%, below broader expectations, though the underlying details relevant for core PCE tracking were mixed to slightly firmer. Following the release, the estimate for March core PCE was revised up modestly to 0.27%, from 0.22% previously. The data therefore did not materially disrupt the broader risk bid, but neither did it provide a clear incremental disinflation signal.

First-quarter earnings season has now begun, with large US banks reporting generally solid headline results. JPMorgan, Citigroup, and Wells Fargo all delivered EPS beats, supported by balance sheet growth, though investor debate remained focused on the quality and sustainability of revenue drivers. JPMorgan appeared to draw the most scrutiny, with key operating metrics around deposits, funding costs, loan growth, and capital markets generally viewed positively, but some disappointment around the lack of an upward revision to core NII guidance. Wells Fargo continues to be viewed by many as a “show-me” story, though desk conversations suggested somewhat warmer underlying tone. BlackRock was viewed more favourably, with bulls arguing that consensus concerns around April 2026 had been cleared and that the stock may still have scope for valuation recovery. Invesco was more actively debated, with some suggesting that reduced need for funding shorts in traditional asset managers could be supportive for peers.

In derivatives, the key feature of the session was spot higher alongside firmer implied volatility. As optimism around Iran helped lift the market, volatility did not fully retrace, suggesting the rally moved through a significant portion of dealer long gamma exposure and may be leaving the street somewhat shorter gamma on further upside. Flow demand was strongest in short-dated S&P and Nasdaq exposure, while there was also increased interest in Technology and Software as clients looked to re-add net exposure. The desk also highlighted demand for Microsoft call spreads into earnings. Into VIX expiry, the preference remains for expressing long volatility through upside structures, with the following session’s straddle marking at approximately 53bp.

The tone in US equities remains constructive. The rally continues to be supported by a combination of improving geopolitical sentiment, lower oil, a softer dollar, strong AI leadership, better long-only demand, and ongoing hedge covering. The fact that volatility has remained relatively firm even as equities move higher suggests upside participation is expanding rather than simply reflecting a low-quality squeeze. Near term, the key question is whether incoming earnings can validate the improving tone in positioning and leadership.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!