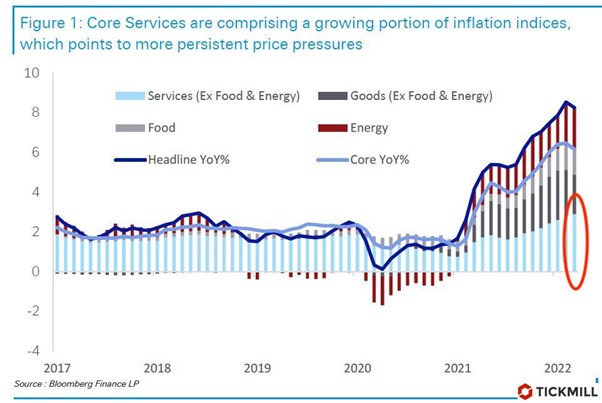

US Inflation Becomes more Persistent and the Fed may be Forced to act Quickly

The release of April US inflation report became the trigger of a new wave of sell-off in risk assets as the magnitude of slowdown and dynamics of the components did not live up to expectations. Headline inflation was 0.6% against the forecast of 0.4%, core inflation was 0.3% against the forecast of 0.2%. The main downward contribution to CPI was made by volatile components - fuel prices and used cars. At the same time, price inflation in core services, which are less volatile from month to month, has accelerated:

The growing contribution of less volatile components to inflation means that inflation is likely to be more persistent than expected. In turn, the Fed will likely have to not only tighten policy faster, but also consider a higher level of interest rate at which the tightening cycle will be completed.

The prospect that the Fed will have to act more aggressively did not sit well with risk assets, with the S&P 500 futures diving below 3900, the lowest since March 2021. The dollar index rose to 104.50, the highest since December 2002. EURUSD broke through 1.04, the Euro has not traded so cheaply against the dollar since January 2017.

Inflation in the US probably peaked in March and will now gradually decline. The question is how quickly this will happen. Manheim data showed that US auto auction prices have declined 6.4% over the past three months, suggesting a further slowdown in used car prices, which account for about 4.1% of the total CPI basket of goods and services. Consumers gradually increase the share of consumption of services and decrease the share of consumption of goods, so the impact of disruptions in supply chains of goods on inflation will gradually decrease. However, the behavior of fuel and services prices remains highly uncertain, in particular, gasoline prices will make significant positive contribution to headline CPI for May and June if geopolitical tensions remain high.

There is every chance that the conflict in Ukraine will drag on until the end of the year and even longer, as active hostilities are reduced and the parties move to a struggle of attrition. In this case, the sanctions pressure on Russia is likely to remain high, which means that tensions in the energy market will persist for a longer time, having a permanent impact on the overall price increase in developed economies.

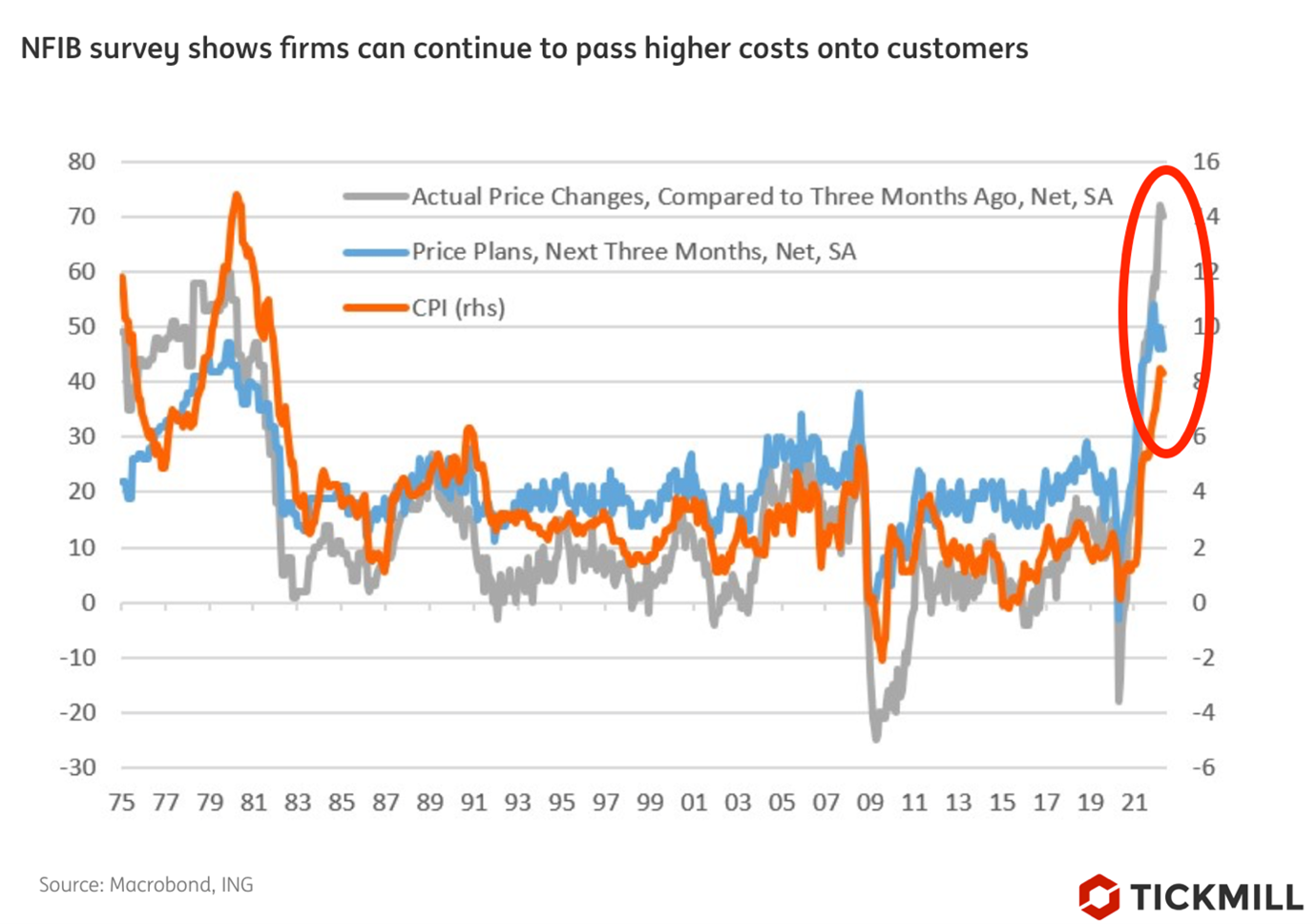

In the US, the price power of firms is also growing, which is another important sign that a rapid decline in inflation is not to be expected. The NFIB Small Business Report showed firms in the US are steadily raising prices, with a record 70% share of respondents reporting higher prices for their goods and services. At the same time, 46% of respondents said that they plan to continue to raise prices.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.