Technical Setup in the Dollar Index Suggests Upside Rebound is in Cards

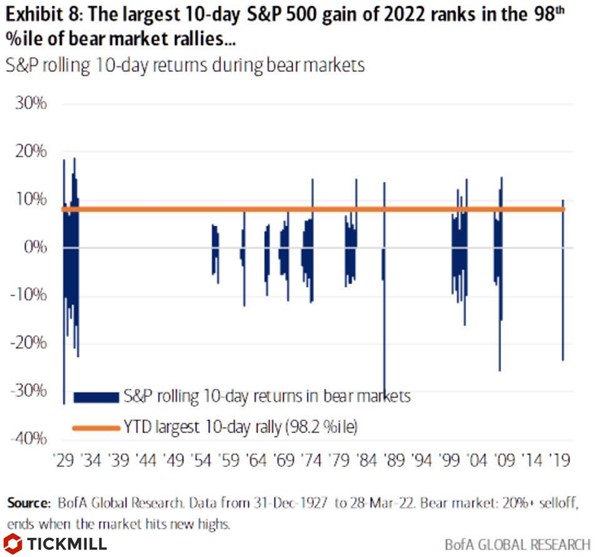

The rebound in SPX over the past 10 days was in the 2% of the strongest bear market rallies (defined as a fall 20%+ from ATH) in nearly 100 years of observations, indicating speculative flows could play a good part in it. According to Nomura strategist McElliott, the rally was fueled by buying frenzy of retail investors, suggesting there is a high risk that the rally isn’t sustainable:

Yesterday SPX added 1.23% in spite of moderately negative background in geopolitics and persistent inflation challenges. European markets do not share the optimism of US indices today - main equity indices bear moderate losses within 1.5%. There is conflicting information on the de-escalation of the conflict in Ukraine: nodding its head initially that, yes, the situation is moving towards a truce, the West later changed its stance and began to interpret the “partial” withdrawal of Russian troops from Kyiv and Chernigov as another maneuver to buy time. Clearly, the surge in risk appetite seen in recent days could be very volatile.

The dollar, within the continuing negative correlation with the US stock market, lost another half a percent today. The situation resembles a long squeeze against the background of the emergence of a clearly-defined catalyst that is easier to interpret by majority of the market (“soon end of the war”) and monetary policy divergence factor is likely to come back into spotlight soon.

The dollar index has formed a nice range of 97.80-99.40 on the daily timeframe as part of a bullish trend. Often this pattern indicates that the trend will continue. Selling of the dollar in the last few days has been rapid, the RSI is approaching the overbought zone. Betting on a false probe lower or a rebound from 97.80 looks an interesting opportunity:

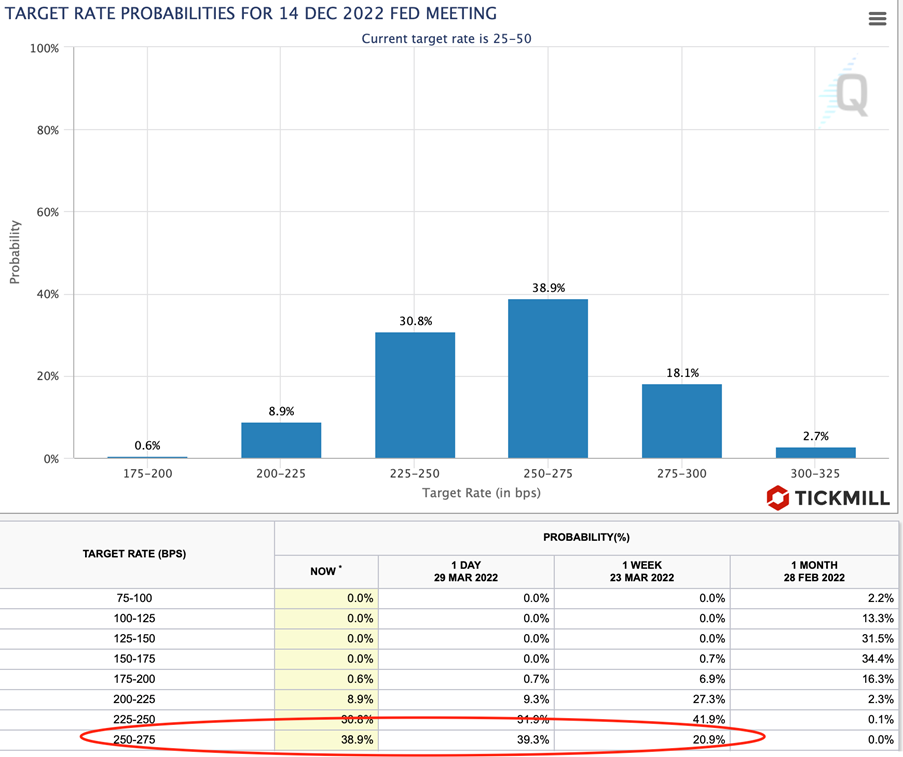

Yesterday's reports on the US economy (Case-Schiller index, JOLTS, Consumer Confidence) refuted hopes that inflation in the US is slowing down. At the same time, the market is strengthening the opinion that the Fed will continue to revise the pace of tightening policy upwards. The gap between Fed-targeted interest rates and inflation expectations has never been so wide – the Consumer Confidence report pointed to household expectations of inflation at 7.9%, while the Fed interest rate is in the range of 25-50 bp. Markets are predicting 9 more rate hikes of 25bp each this year (i.e. range 250-275 at the end of the year):

The head of the Central Bank of England, Bailey, in his speech yesterday warned that the British economy is sliding into stagflation - a state characterized by low rates of real output and high inflation. He called the ordeal Brits are facing a historic shock to real incomes. The Central Bank is really in a dilemma: if the rate of real output (real income growth) is already low) how to contain inflation by tightening policy without sending the economy into recession? In the second quarter, according to the forecasts of the Central Bank, inflation will accelerate to 8%. Nevertheless, the Central Bank is betting that price growth will begin to slow down at the end of this year (the timing has already been shifted more than once). The easing position of the Central Bank will probably remind the pound sterling more than once.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.