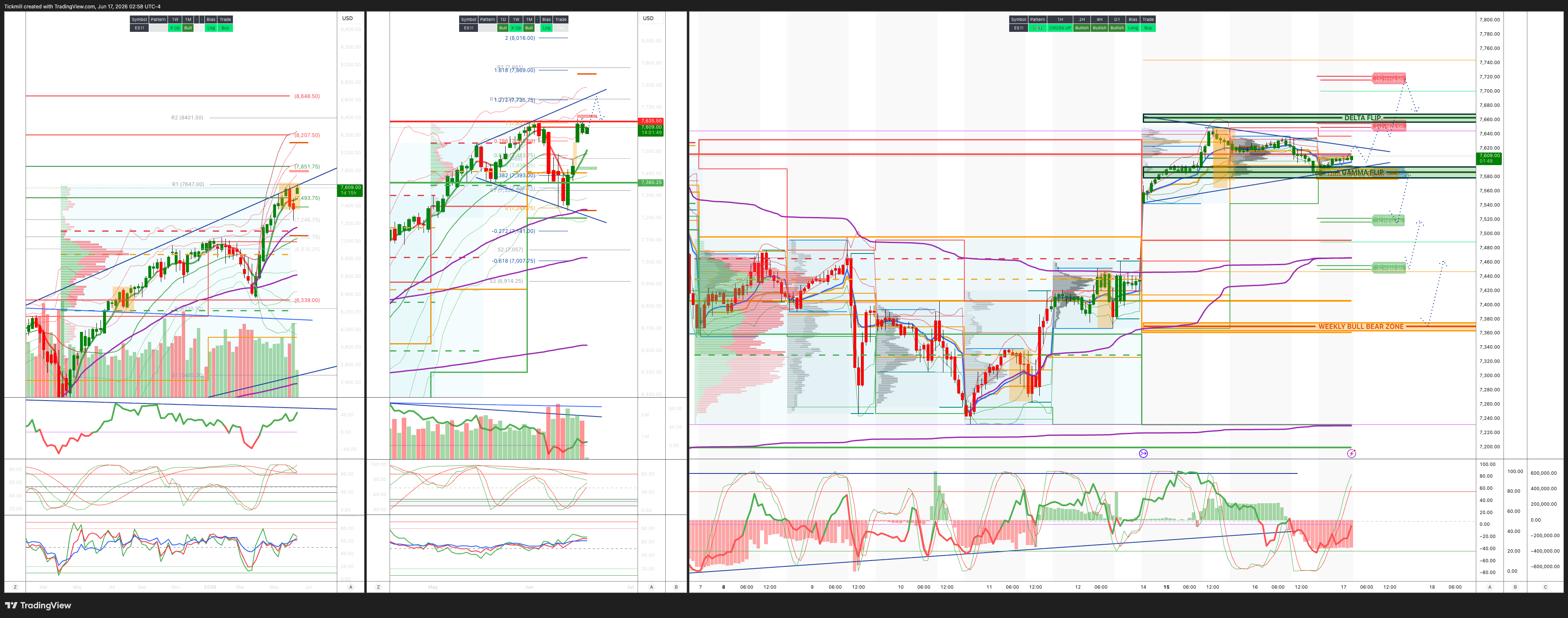

S&P500 Daily Action Areas & Price Targets 17/6/26

S&P500 Daily Action Areas & Price Targets 17/6/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7365/75

WEEKLY RANGE RES 7635 SUP 7360

June MOPEX Straddle: 274pt range implies a OPEX to OPEX range of [7134, 7683]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.29 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7439

WEEKLY VWAP BEARISH 7474

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - BALANCE - 7648/7583

WEEKLY STRUCTURE - OTFH

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7570/60 ACTIVE FROM YESTERDAY’S REJECT/RECLAIM

GAMMA FLIP 7589

DELTA FLIP 7665

DAILY RANGE RES 7651 SUP 7515

2 SIGMA RES 7719 SUP 7447

VIX BULL BEAR ZONE 19

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET 7630 > DAILY RANGE RES

SHORT ON REJECT/RECLAIM DAILY RANGE RES TARGET 7630

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Rising Tide’

The market took a breather after the aggressive risk-on move, with the S&P down 57bps to 7,511, the NDX down 189bps to 29,968, the Russell down 87bps to 2,939, and the Dow up 64bps to 51,999. Volumes remained elevated at 21.073bn shares versus a YTD daily average of 19.313bn, but floor activity was quiet at 4 out of 10. The tape felt more like profit-taking and consolidation than a material deterioration in the broader risk backdrop, especially with oil down nearly 5%, yields lower, and VIX only modestly higher to 16.41.

The main pressure point was Tech, particularly Semis, which fell around 5% after a roughly 14% three-day rally. That looks more like healthy consolidation after a violent rebound than a definitive break in the AI trade. Mega-Cap Tech supply remained visible, with asset managers slight net sellers driven by continued supply in Mega-Cap Tech, while hedge funds were about $2bn net sellers, led by Communication Services and Info Tech, with elevated shorting activity. The fact that the Dow finished higher while NDX lagged reinforces the idea that this was a rotation/profit-taking session rather than broad de-risking.

SPCX was the standout speculative pocket, closing at $201 and continuing to power higher. There may be a shift in retail activity from trading Semis into trading SPCX, with retail and indexers seemingly on the bid and options activity adding fuel. On its first day of options trading, SPCX saw 1.72mm contracts trade, with about 57% of volume in calls. Institutional flows were two-way and, on balance, skewed better for sale today, which suggests the marginal excitement is coming more from retail/options/indexer demand than from clean institutional accumulation.

The cross-asset setup remains supportive for parts of the market outside crowded Tech. The 10-year yield fell to 4.4375%, which continues to help Alts, Homebuilders, and other rate-sensitive groups. Crude fell another 4.95% to $76.74 ahead of the expected US/Iran peace deal signing on Friday. That is a major macro relief valve, especially after the prior inflation and geopolitical risk premium. Lower oil supports disinflation, consumer real income, margins, and the Fed’s ability to stay patient.

GIR’s revised Brent forecasts reinforce the energy disinflation story. They cut their 2026Q4 Brent forecast to $80 from $90 and their 2027 average forecast to $75 from $80. They now expect Persian Gulf exports to normalize to pre-war levels by the end of July rather than the end of August. If that proves right, the market can take a meaningful energy shock off the table. The key question is whether lower crude becomes a durable boost to risk assets or starts to signal softer demand. For now, equities are treating it primarily as a positive supply/geopolitical relief story.

The big event is now the first FOMC under Chair Warsh. The market expects no rate change, so the focus is entirely on communication. With oil collapsing and yields easing, Warsh has room to sound patient, but inflation data are still not clean enough for a dovish victory lap. The market will be sensitive to whether he emphasizes no cuts this year and inflation credibility, or whether he frames recent inflation pressure as partly supply-driven and less responsive to demand-side tightening. The same hold decision could produce very different outcomes depending on the tone of the press conference.

Liquidity remains a concern. Top-of-book depth is now just $2.69mm, down about 20% versus the 20-day moving average. That is very poor for an index sitting near highs and heading into a major Fed event. Thin liquidity means flow imbalances can create outsized price moves, and it also increases the value of owning convexity. The market can appear calm with VIX in the mid-16s, but beneath the surface the ability to absorb shocks is reduced.

The derivatives session was calmer, with spot and vol trading positively correlated and front-end vol ultimately closing lower across the three major indices. Skew steepened across the board as spot moved lower, which is normal after the sharp vol crush and small equity pullback. The desk views VIX call spreads as attractive after the volatility compression of the past week, especially July and August structures. That makes sense because they provide a cleaner hedge against a summer vol reset without requiring constant re-striking, and they avoid paying for outright convexity at the most inefficient points.

For SPCX, elevated implied volatility argues for call spreads rather than outright calls for upside expression. When retail demand and call activity are intense, outright calls can be expensive and decay quickly if momentum stalls. Call spreads better match the tactical nature of the trade by monetizing high vol and defining upside. The desk also remained active in collars and overwrites on existing long positions, which fits the broader environment: investors still want to own winners, but they increasingly want to monetize call skew or finance downside protection after large moves.

The implied move for tomorrow is 0.74%, which is meaningful given the Fed event and the recent decline in front-end vol. The setup is asymmetric in the sense that a steady, patient Warsh could allow the market to stabilize and continue the broadening/rate-sensitive rally, while a more hawkish Warsh could pressure front-end rates and re-hit NDX, Semis, and other long-duration exposures. With Tech still seeing supply and liquidity poor, the market is vulnerable to communication missteps even though the macro backdrop from oil and rates is favorable.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!