Chart of the Day GBPUSD

Chart of the Day GBPUSD

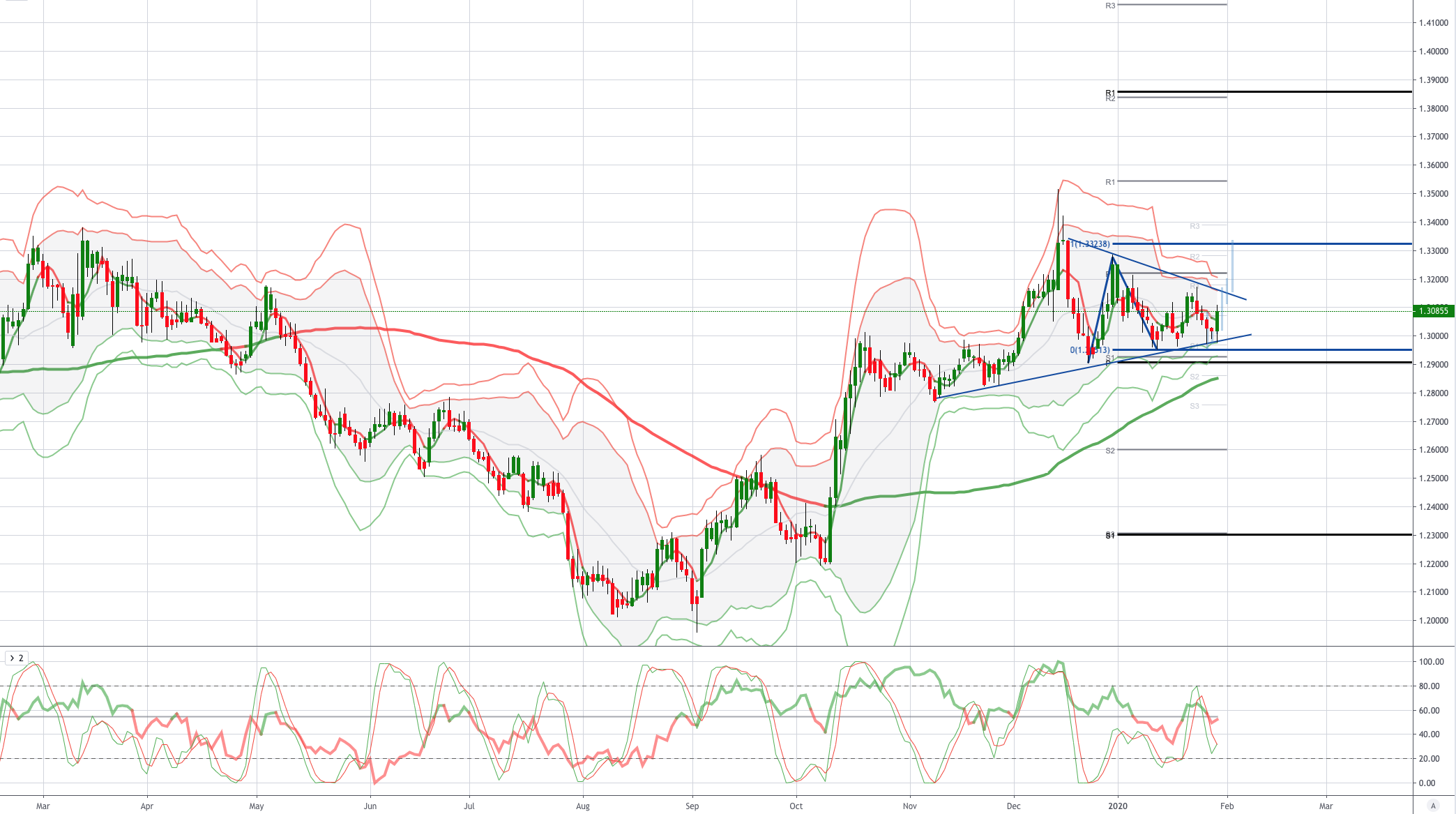

Potential upside GBPUSD

GBPUSD In Governor Carney’s final meeting, the Bank of England’s Monetary Policy Committee (MPC) voted 7-2 in favour of keeping policy unchanged – leaving Bank Rate at 0.75%; the size of the Asset Purchase Facility at £435bn; and the stock of corporate bond purchase at £10bn. While this was in line with our expectations, recent commentary from a number of MPC members (including Carney), alluding to the possibility of supporting the two members of the MPC currently looking for a rate cut, along with a spate of weaker-than-expected data releases, had led markets to see a significant risk of a cut at today’s meeting. In particular, after the release of the December retail sales report, the probability that markets attached to a January rate cut rose to around 70%. While this had dropped back in recent days, the prospect of a cut at today’s meeting was still viewed as a 50/50 outcome.

The fact that the BoE chose not to reduce interest rates at the January MPC meeting is not particularly surprising given our reading of the various speeches/interviews – which triggered the initial move higher in expectations of a rate cut in recent weeks. While a trio of BoE officials, Silvana Tenreyro, Gertjan Vlieghe and Governor Carney, highlighted a willingness to vote for an immediate reduction in rates, this was very much contingent on incoming survey evidence not supporting the notion of a post-election bounce in confidence

In the end, the subsequent release of a number of strong sentiment gauges, including the PMIs, CBI Industrial Trends, Deloitte CFO, and the RICS housing survey, all showed a relatively sharp turnaround in domestic sentiment and suggested that the economy was in the midst of a post-election rebound, and provided strong grounds not to switch and support the other two members of the MPC, Jonathan Haskel and Michael Saunders, who had been looking for an immediate reduction since November. From here, the prospect of a near-term cut in interest rates rests on a number of factors, not least whether the evolution of the hard data supports the view that economic activity has bounced back strongly post the election result. On the assumption that the improvement in confidence is sustained, and borne out in the forthcoming economic data, this should eventually lessen the case for a looser monetary policy stance.

It is therefore prudent for the MPC to wait and assess the full impact of the post-election recovery in economic confidence, particularly with full details of the expected fiscal stimulus measures in the Budget on 11th March yet to be revealed, and the UK set to embark on negotiations with the EU on the future relationship in the coming months, which may also change the broad contours of the UK’s growth outlook.

From a technical and trading perspective,GBPUSD has failed to sustain closing downside breaches of 1.30 on multiple tests. Today’s bullish reversal candle could be the catalyst for a further extension to the upside, the first pivotal resistance comes in around 1.3160, through here and bulls will initially be setting sites on an equidistant swing objective sited at 1.3327, a closing topside breach of this level will expose the post election spike high at 1.35 and likely stops above this level.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73% and 70% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!